Developing markets share several problems in common. One such problem is the inability of most people to have full access or any access at all to the financial system. For example, the unbanked have no access to the traditional system, they are unable to create accounts or use the services of banks, and the underbanked do not have sufficient access to mainstream financial services such as credit and loans. These groups are predominant on the African continent, making it a hotbed for innovation in the financial technology sector. In recent times, the fintech world has embraced cryptocurrencies as an important addition to further the mission of making finance accessible to all. This article examines how crypto intersects with fintech in Africa to enable development.

The latest data published by McKinsey & Company shows that out of 5,200 tech companies started in Africa between 2021 and 2022, just under half of them are fintech start-ups. Most of these companies seek to disrupt or provide an additional layer to traditional finance. The African traditional finance space is well developed in some parts. In very vibrant countries, simple services like bank accounts and debit cards are readily available. Mobile money services also provide an upgrade in key markets like Ghana and Kenya, where everyone can have a “bank account” tied to their mobile number. This has made it easier for people to transact and created a near cashless environment, especially in urban areas. Despite the availability of these basic services, developing economies need a lot more than the bare minimum to empower their citizens.

Not every country can boast of these basic services. In some parts, financial accounts are still scarce, and people have no option but to carry loads of cash and rely on their own security for their money. Fintech companies on the continent intend to fill the gap by providing services for those with none and improve on the offerings provided for the masses.

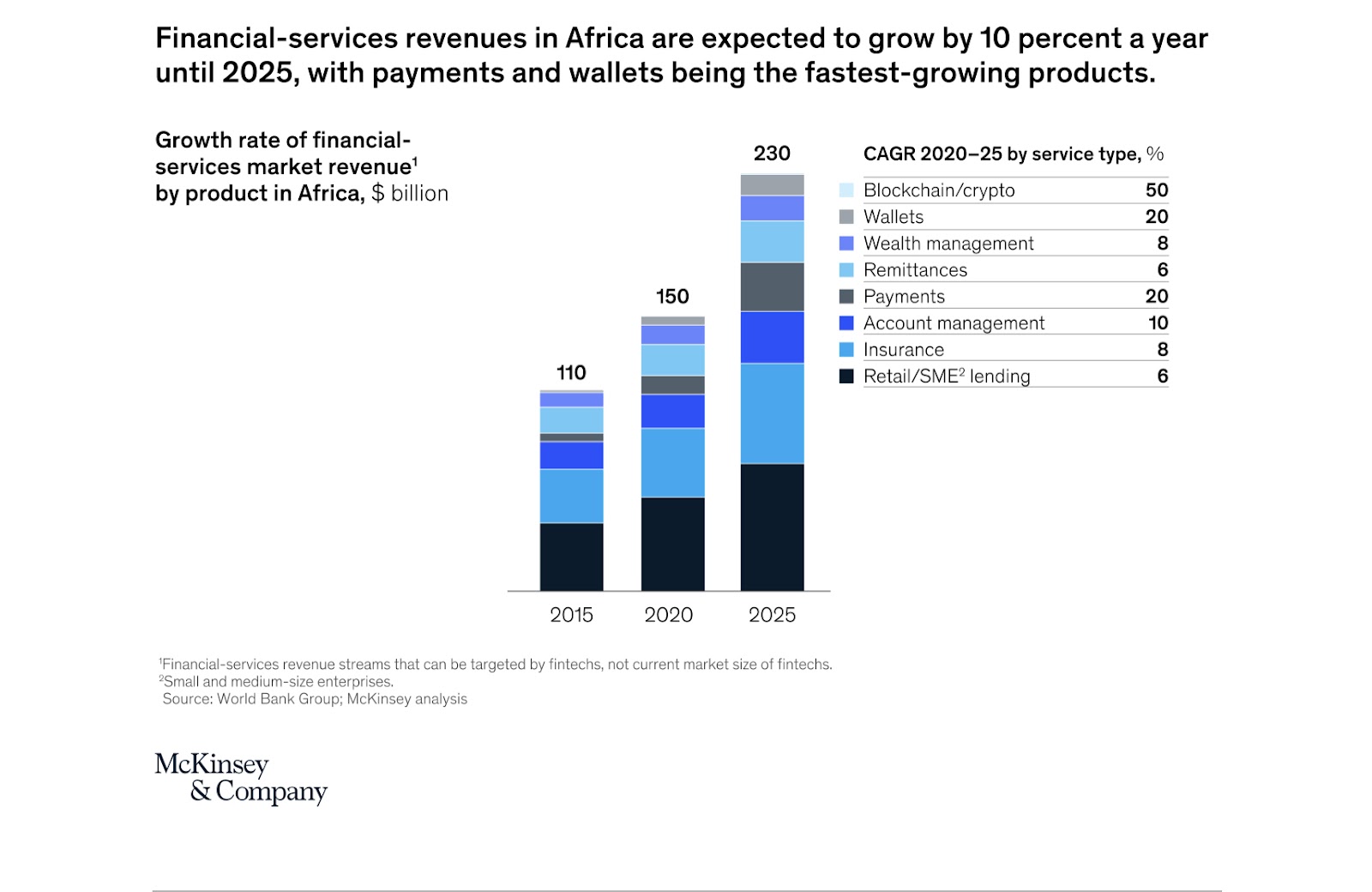

Significant issues that fintech applications in Africa seek to solve include payments and remittances, wealth management, insurance, retail and small-scale enterprise (SME) lending, and improvements in the operation and infrastructure of finance. This is where cryptocurrencies come in. Most, if not all, of the changes fintech innovators intend to tackle are at the heart of the cryptocurrency ethos. What’s more, the existence of decentralized currencies provides an avenue for fintech companies to break away from the limitations of traditional financial systems. The realization of the flexibility cryptocurrency provides fintech applications, has led to the boom in the creation of new tools and services that incorporate both worlds. McKinsey & Company, in its latest “Fintech in Africa: The end of the beginning” report, projected that revenue for African fintech companies is likely to grow by 10 percent per year to reach approximately $230 billion by 2025. Within this, the blockchain and crypto sector is expected to grow the fastest at around 50 percent CAGR from 2020 – 2025.

The exponential growth of crypto as part of the broader fintech industry is due to the connection between crypto and all other sub-sections of fintech. Here are the various ways fintech and crypto meet:

Remittance is an important foreign earner for the continent. The ability to receive and send international payments on the continent has largely been outsourced to foreign solutions that are not readily available in most instances or cost an arm and a leg when they work. For instance, Western Union and MoneyGram charge high fees for the smallest transactions. Fintech applications intend to change that by creating platforms that make remittance easier for the average African. The problem with international transfers may not be the existence of apps per se but the use of traditional systems to facilitate transfers. Moving money from one bank account in one country to another can be more complex than it seems. On the other hand, cryptocurrencies require less infrastructure and are easy to move around. This has led to several payment applications integrating cryptocurrency wallets. Chipper Cash, one of the biggest fintech apps in Africa, added Bitcoin support in November 2020. This move has made the app very popular as it became a bridge between traditional finance and decentralized finance. Chipper Cash also attracted funding from crypto giants FTX as a result of this strategic decision. A similar trend is happening with wallets and payments. Since most fintech applications in Africa combine payments, wallets, and remittances, the integration of crypto by these applications is equally bringing upgrades to those areas.

Another important trend to note is the addition of fintech features by crypto applications. The merger between both sectors is not a one-way street as crypto platforms also intend to capture some market share from traditional fintech applications. For instance, Binance rolled out Binance Pay on the African continent recently, allowing users to send money from one Binance user to another without using cryptocurrency addresses or a crypto native interface. The extension of the exchange platform’s features also allows users to pay bills and purchase airtime or data packages like most fintech apps that focus on payments and wallet management do.

Wealth management is another aspect of finance that is expected to become very popular as the middle class on the continent shifts towards more modern forms of investments. Some fintech applications are creating space for speculative trading with the introduction of stock markets and spot crypto trading on their platforms. These alternative investments have become attractive due to the poor performance of currencies on the continent. Another part of finance that could use an upgrade on the continent is the availability of loans and capital. The decentralized finance (DeFi) space has found more innovative ways to provide loans and how to deal with issues about credit. DeFi loans or crypto-powered loans are yet to take off as part of fintech offerings, but it may be a defining feature for crypto adoption.

As fintech companies continue to grow due to the increase in smartphone ownership, expansion of internet access, reduction of internet cost, and a young and urban population, the chances of seeing more integration between the fintech and crypto sectors is set to increase.